2019/20 | Responsible Investment Report

As a UN-supported Principles for Responsible Investment (PRI) signatory and formal supporter of the Financial Stability Board Task Force on Climate-related Financial Disclosures (TCFD), we recognise the value in being clear about our Responsible Investment (RI) strategy and sharing what we are doing.Contents

Responsible Investment Report 2019/20

wwwwww.ppf.ppf..coco.uk.uk RResponsibesponsible Inle Invvestment Restment Report 2eport 200119/29/200 1 A p p r Contents o As a UN-supported Principles ach for Responsible Investment Part 1: Approach 2 Aim of the Responsible Investment Report 4 (PRI) signatory and formal Executive summary 6 Leadership statements 8 supporter of the Financial Stability The foundations of our RI principles 12 Our RI approach 14 E x e Board Task Force on Climate- c u t ion related Financial Disclosures Part 2: Execution 18 Being active owners 20 (TCFD), we recognise the value in Managing climate change risks and opportunities 30 being clear about our Responsible Investment (RI) strategy and Part 3: Looking forward 38 L o Continuing to drive RI forward 40 ok in g sharing what we are doing. Meet the team 42 f o r w ar d

wwwwww.ppf.ppf..coco.uk.ukRResponsibesponsible Inle Invvestment Restment Report 2eport 200119/29/200 1 A p p r Contents o As a UN-supported Principles ach for Responsible Investment Part 1: Approach 2 Aim of the Responsible Investment Report 4 (PRI) signatory and formal Executive summary 6 Leadership statements 8 supporter of the Financial Stability The foundations of our RI principles 12 Our RI approach 14 E x e Board Task Force on Climate- c u t ion related Financial Disclosures Part 2: Execution 18 Being active owners 20 (TCFD), we recognise the value in Managing climate change risks and opportunities 30 being clear about our Responsible Investment (RI) strategy and Part 3: Looking forward 38 L o Continuing to drive RI forward 40 ok in g sharing what we are doing. Meet the team 42 f o r w ar d

2 www.ppf.co.uk Responsible Investment Report 2019/20 3 A ppr oa c Approach h E x e c u t ion L o o k in g f o r w ar d

2www.ppf.co.ukResponsible Investment Report 2019/20 3 A ppr oa c Approach h E x e c u t ion L o o k in g f o r w ar d

4 www.ppf.co.uk Responsible Investment Report 2019/20 5 Aim of the Responsible Investment Report A ppr oa c h E x e c u t ion 1 2 3 L o o k in g f In part 1 of this report we In part 2, we outline the Part 3 looks forward o r w Responsible investing and the integration outline who we are, why we execution of our key to future developments ar of environmental, social and governance believe being a responsible priorities in being active planned for 2020/21 d Responsible (ESG) factors have been embedded in our investor is important, and owners and managing and beyond. investment is investment process since our inception. how we endeavour to act climate change risks and an important In 2018 we enhanced and formalised responsibly in our day-to-day opportunities. This also commitment in our RI framework. Since then, we have investment activities. covers our commitment to our Strategic Plan. focused on applying the framework across investor collaboration, which is critical to the success I’m delighted to both internally and externally-managed of the wider industry, as introduce our portfolios. together, we are better inaugural RI report, equipped to meet the As a UN-supported Principles for challenges facing us. which sets out our Responsible Investment (PRI) signatory RI strategy and and formal supporter of the Financial progress so far. Stability Board Task Force on Climate- related Financial Disclosures (TCFD), we recognise the value in being clear Oliver Morley, CEO about our RI strategy and sharing what we are doing. 06-17 18-37 38-42

4www.ppf.co.ukResponsible Investment Report 2019/20 5 Aim of the Responsible Investment Report A ppr oa c h E x e c u t ion 1 2 3 L o o k in g f In part 1 of this report we In part 2, we outline the Part 3 looks forward o r w Responsible investing and the integration outline who we are, why we execution of our key to future developments ar of environmental, social and governance believe being a responsible priorities in being active planned for 2020/21 d Responsible (ESG) factors have been embedded in our investor is important, and owners and managing and beyond. investment is investment process since our inception. how we endeavour to act climate change risks and an important In 2018 we enhanced and formalised responsibly in our day-to-day opportunities. This also commitment in our RI framework. Since then, we have investment activities.covers our commitment to our Strategic Plan. focused on applying the framework across investor collaboration, which is critical to the success I’m delighted to both internally and externally-managed of the wider industry, as introduce our portfolios. together, we are better inaugural RI report, equipped to meet the As a UN-supported Principles for challenges facing us. which sets out our Responsible Investment (PRI) signatory RI strategy and and formal supporter of the Financial progress so far. Stability Board Task Force on Climate- related Financial Disclosures (TCFD), we recognise the value in being clear Oliver Morley, CEO about our RI strategy and sharing what we are doing. 06-17 18-37 38-42

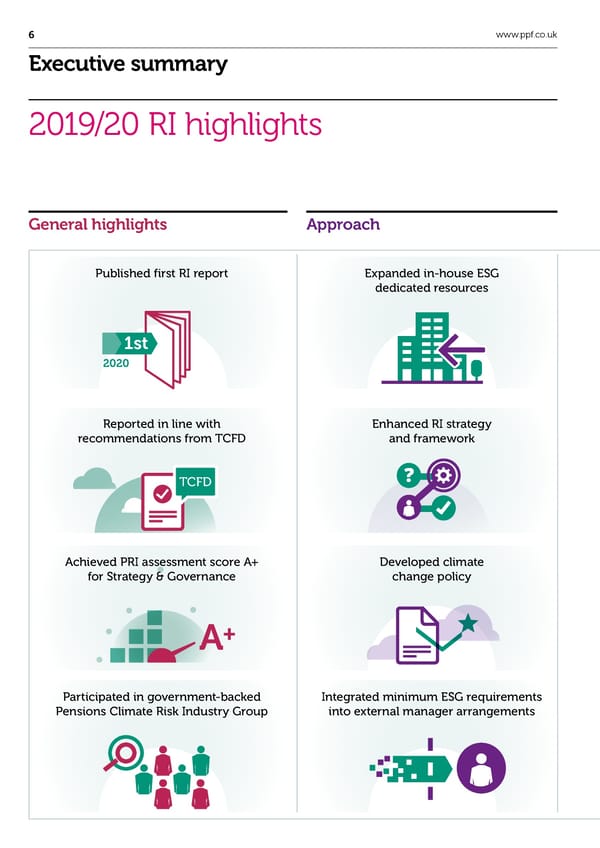

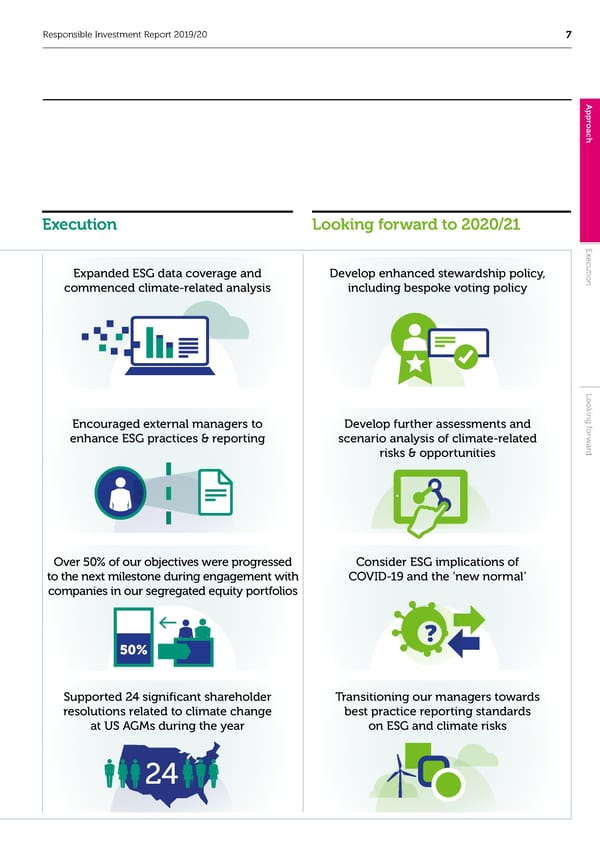

6 www.ppf.co.uk Responsible Investment Report 2019/20 7 Executive summary A ppr oa 2019/20 RI highlights c h General highlights Approach Execution Looking forward to 2020/21 E x e c u t Published first RI report Expanded in-house ESG Expanded ESG data coverage and Develop enhanced stewardship policy, ion dedicated resources commenced climate-related analysis including bespoke voting policy 1st 2020 L o o k in g Reported in line with Enhanced RI strategy Encouraged external managers to Develop further assessments and f o r recommendations from TCFD and framework enhance ESG practices & reporting scenario analysis of climate-related w ar risks & opportunities d TCFD Achieved PRI assessment score A+ Developed climate Over 50% of our objectives were progressed Consider ESG implications of for Strategy & Governance change policy to the next milestone during engagement with COVID-19 and the ‘new normal’ companies in our segregated equity portfolios + A 50% Participated in government-backed Integrated minimum ESG requirements Supported 24 significant shareholder Transitioning our managers towards Pensions Climate Risk Industry Group into external manager arrangements resolutions related to climate change best practice reporting standards at US AGMs during the year on ESG and climate risks 24

6www.ppf.co.ukResponsible Investment Report 2019/20 7 Executive summary A ppr oa 2019/20 RI highlights c h General highlightsApproachExecution Looking forward to 2020/21 E x e c u t Published first RI report Expanded in-house ESG Expanded ESG data coverage and Develop enhanced stewardship policy, ion dedicated resourcescommenced climate-related analysis including bespoke voting policy 1st 2020 L o o k in g Reported in line with Enhanced RI strategy Encouraged external managers to Develop further assessments and f o r recommendations from TCFDand frameworkenhance ESG practices & reporting scenario analysis of climate-related w ar risks & opportunities d TCFD Achieved PRI assessment score A+ Developed climate Over 50% of our objectives were progressed Consider ESG implications of for Strategy & Governance change policyto the next milestone during engagement with COVID-19 and the ‘new normal’ companies in our segregated equity portfolios + A 50% Participated in government-backed Integrated minimum ESG requirements Supported 24 significant shareholder Transitioning our managers towards Pensions Climate Risk Industry Groupinto external manager arrangements resolutions related to climate change best practice reporting standards at US AGMs during the year on ESG and climate risks 24

8 www.ppf.co.uk Responsible Investment Report 2019/20 9 Leadership statements A ppr Chair’s foreword oa c h On behalf of the Board, I am We take all our responsibilities UK pensions sector, as one of the E x e pleased to reaffirm our commitment seriously and, despite our continued world’s largest investor groups c u t RI has always been to RI at the PPF. We have been success, we will never permit representing £1.6 trillion of assets, ion responsible stewards since the PPF ourselves to become complacent. should be a leader on this. The UK’s at the core of how was established 15 years ago, and Recognising these responsibilities, enhanced regulations provide a we do things and I signatories to the PRI since 2007. we look to emulate best practice significant opportunity to strengthen We pride ourselves on being a stable in governance and regulation. We how its pensions industry is taking am delighted that, organisation with strong principles fully support the guidance of the ESG factors into account and and values, and we are committed to TCFD, and our response to the reporting on them, particularly for with a lot of work continuing to protect our members recommendations is reflected in climate-related issues. Over the past done behind the for many years to come. the 2019/20 Annual Report and year, we have enjoyed working with Accounts. the DWP and The Pensions Regulator As a long-term investor, we look to be (TPR), among other participants, as a L scenes, we are now o vigilant and remain agile to all market We also believe in strong peer member of the Pensions Climate Risk o k publishing our dynamics and evolving global trends – collaboration across the industry, Industry Group. Its objective is to in g f including climate change – to identify both with other asset owners support UK schemes on this journey, o r inaugural RI report. risks and opportunities. In order to and our external managers. We and we hope that the new Pension w ar serve our members, and provide for welcomed the recent regulatory Schemes Bill will also be a driver for d our levy payers and other stakeholders, amendments by the Department continuing progress. we take a strong and informed stand for Work and Pensions (DWP) that on responsible investing. It is a priority, clarified the requirements for UK We have no doubt that the as set out in our Strategic Plan. With Occupational Pension Schemes. importance of being a responsible regular updates from the Investment These included incorporating asset owner will only grow. This report Team and its dedicated ESG specialists, financially material environmental, presents our progress so far and our the Board is well informed and able social and governance (ESG) commitment to continue evolving. to provide oversight and steer on considerations into their approach, the evolution of our RI framework and we acknowledge the long- Our RI journey so far and activities. term benefits they will deliver. The Arnold Wagner, OBE 2005–2020 April 6 – February 16 – Became signatory to the RI criteria formally Board adopted Statement of ESG research Became member First RI report We opened became signatory to the Carbon Disclosure Project embedded in Stewardship principles and Standard provider appointed of IIGCC and formal published; TCFD our doors UN-supported PRI and (CDP); RI ratings process manager selection of Diligence; RI Manager chaired the supporter of TCFD and aligned reporting used principles as base for developed process; became PRI’s Fixed Income workstream and Climate Action 100+ defining our core RI beliefs member of UKSIF led collaboration of UK pension funds to standardise expectations for ESG disclosures from listed equity managers 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 20 005 006 0 0 009 010 01 01 01 0 01 01 01 01 01 07 08 1 2 3 14 5 6 7 8 9 20 Voting & Engagement RI principles enhanced within RI clauses formally RI minimum standards policy RI enhanced framework overlay service acquired Statement of Investment included in investment approved; responded to DWP and new climate change Principles; responded to management agreements, consultation on changes policy approved; became the FRC’s consultation on a based on best practice to Investment Regulations, formal supporter of new UK Stewardship Code defined by International following the Law Commission Transition Pathway and issued statement of Corporate Governance report on Fiduciary Duty Initiative; joined Pensions compliance in Sep 2010 Network (ICGN) Climate Risk Industry Group

8www.ppf.co.ukResponsible Investment Report 2019/20 9 Leadership statements A ppr Chair’s foreword oa c h On behalf of the Board, I am We take all our responsibilities UK pensions sector, as one of the E x e pleased to reaffirm our commitment seriously and, despite our continued world’s largest investor groups c u t RI has always been to RI at the PPF. We have been success, we will never permit representing £1.6 trillion of assets, ion responsible stewards since the PPF ourselves to become complacent. should be a leader on this. The UK’s at the core of how was established 15 years ago, and Recognising these responsibilities, enhanced regulations provide a we do things and I signatories to the PRI since 2007. we look to emulate best practice significant opportunity to strengthen We pride ourselves on being a stable in governance and regulation. We how its pensions industry is taking am delighted that, organisation with strong principles fully support the guidance of the ESG factors into account and and values, and we are committed to TCFD, and our response to the reporting on them, particularly for with a lot of work continuing to protect our members recommendations is reflected in climate-related issues. Over the past done behind the for many years to come. the 2019/20 Annual Report and year, we have enjoyed working with Accounts. the DWP and The Pensions Regulator As a long-term investor, we look to be (TPR), among other participants, as a L scenes, we are now o vigilant and remain agile to all market We also believe in strong peer member of the Pensions Climate Risk o k publishing our dynamics and evolving global trends – collaboration across the industry, Industry Group. Its objective is to in g f including climate change – to identify both with other asset owners support UK schemes on this journey, o r inaugural RI report. risks and opportunities. In order to and our external managers. We and we hope that the new Pension w ar serve our members, and provide for welcomed the recent regulatory Schemes Bill will also be a driver for d our levy payers and other stakeholders, amendments by the Department continuing progress. we take a strong and informed stand for Work and Pensions (DWP) that on responsible investing. It is a priority, clarified the requirements for UK We have no doubt that the as set out in our Strategic Plan. With Occupational Pension Schemes. importance of being a responsible regular updates from the Investment These included incorporating asset owner will only grow. This report Team and its dedicated ESG specialists, financially material environmental, presents our progress so far and our the Board is well informed and able social and governance (ESG) commitment to continue evolving. to provide oversight and steer on considerations into their approach, the evolution of our RI framework and we acknowledge the long- Our RI journey so farand activities. term benefits they will deliver. The Arnold Wagner, OBE 2005–2020 April 6 – February 16 – Became signatory to the RI criteria formally Board adopted Statement of ESG research Became member First RI report We opened became signatory to the Carbon Disclosure Project embedded in Stewardship principles and Standard provider appointedof IIGCC and formal published; TCFD our doorsUN-supported PRI and (CDP); RI ratings process manager selection of Diligence; RI Manager chaired the supporter of TCFD and aligned reporting used principles as base for developedprocess; became PRI’s Fixed Income workstream and Climate Action 100+ defining our core RI beliefsmember of UKSIFled collaboration of UK pension funds to standardise expectations for ESG disclosures from listed equity managers 22222222 2 2 2 2 2 2 2 20 005006000090100101 01 0 01 01 01 01 01 070812 3 14 5 6 7 8 9 20 Voting & Engagement RI principles enhanced within RI clauses formally RI minimum standards policy RI enhanced framework overlay service acquiredStatement of Investment included in investment approved; responded to DWP and new climate change Principles; responded to management agreements, consultation on changes policy approved; became the FRC’s consultation on a based on best practice to Investment Regulations, formal supporter of new UK Stewardship Code defined by International following the Law Commission Transition Pathway and issued statement of Corporate Governance report on Fiduciary Duty Initiative; joined Pensions compliance in Sep 2010Network (ICGN) Climate Risk Industry Group

10 www.ppf.co.uk Responsible Investment Report 2019/20 11 Leadership statements – continued A ppr Chief Investment Officer’s Overview of the PPF oa c h statement E Our duty is to protect the millions x e c of people who belong to UK defined u t We believe it is vital that we demonstrate a benefit (DB) pension schemes. When ion robust and effective approach to RI, and we these schemes fail, we’re here to see the integration of material ESG issues as support their members. an essential part of the investment process When an employer becomes insolvent and its pension at the PPF. scheme cannot afford to pay its promised pensions, we compensate scheme members for the pensions they have lost. We take over responsibility for payments once we have assessed that a scheme L cannot afford to buy benefits from an insurance o o company which are equal to, or more than, the PPF k Our unique investment strategy Best practice around ESG One area that we are pushing in would pay. Currently around 277,000 people are g f has always been rooted in prudent implementation in some asset strongly is increased disclosure and o members of the PPF. Before the PPF, these people r risk-taking with a focus on generating classes and investment strategies reporting. At present, the level of w could have faced significant financial uncertainty and ar sustainable long-term returns, and is still developing, so we work in fund-specific ESG reporting provided hardship. We protect more than 10 million members d RI is a core component of this partnership with our external by many external managers is of more than 5,000 DB pension schemes. strategy. managers and incentivise them limited, and we will not be able to to evolve their processes. Due to fully deliver on our own reporting I am pleased that our ESG our size, we have the opportunity requirements without underlying How we are funded capabilities have grown in the to encourage improvements in transparency from our external past year, with an additional ESG ESG integration across the globe, managers. In the meantime, to We raise the money we need to pay PPF benefits specialist joining the Investment and we see this as an area where obtain a thorough oversight of and the cost of running the PPF in four ways: Team to support our Head of we can have the most influence. our portfolios in relation to ESG 11% ESG. We have also expanded We have also established a set of risks and opportunities, we are our access to available ESG data, minimum requirements around ESG investing significantly in expertise to insights and analytics, which allow integration and stewardship, and monitor these portfolios ourselves. Split of funding sources us to better track, monitor and will ensure that our expectations Whilst challenging, we recognise Assets from pension schemes ultimately report on various risks are met in order to continue that a tailored approach is often transferred to us and opportunities. Applying the relationships with our external necessary as different schemes The return we make on our TCFD’s recommendations has been managers. will have different characteristics 22.5% 40.5% a key area of focus, as we continue and expectations. The momentum investments to integrate climate-related risk around ESG integration has built The levy we charge on eligible assessment and management. in recent years, yet we are still in pension schemes the early stages of the journey, and Recovered assets we secure recognise that all partners must from insolvent employers work together to deliver on this successfully. We have £32 billion in our investment portfolio Barry Kenneth (31 March 2019) which is continually growing, and is 26% currently managed both internally and externally. Source: The PPF

10www.ppf.co.ukResponsible Investment Report 2019/20 11 Leadership statements – continued A ppr Chief Investment Officer’s Overview of the PPF oa c h statement E Our duty is to protect the millions x e c of people who belong to UK defined u t We believe it is vital that we demonstrate a benefit (DB) pension schemes. When ion robust and effective approach to RI, and we these schemes fail, we’re here to see the integration of material ESG issues as support their members. an essential part of the investment process When an employer becomes insolvent and its pension at the PPF.scheme cannot afford to pay its promised pensions, we compensate scheme members for the pensions they have lost. We take over responsibility for payments once we have assessed that a scheme L cannot afford to buy benefits from an insurance o o company which are equal to, or more than, the PPF k Our unique investment strategy Best practice around ESG One area that we are pushing in would pay. Currently around 277,000 people are g f has always been rooted in prudent implementation in some asset strongly is increased disclosure and o members of the PPF. Before the PPF, these people r risk-taking with a focus on generating classes and investment strategies reporting. At present, the level of w could have faced significant financial uncertainty and ar sustainable long-term returns, and is still developing, so we work in fund-specific ESG reporting provided hardship. We protect more than 10 million members d RI is a core component of this partnership with our external by many external managers is of more than 5,000 DB pension schemes. strategy.managers and incentivise them limited, and we will not be able to to evolve their processes. Due to fully deliver on our own reporting I am pleased that our ESG our size, we have the opportunity requirements without underlying How we are funded capabilities have grown in the to encourage improvements in transparency from our external past year, with an additional ESG ESG integration across the globe, managers. In the meantime, to We raise the money we need to pay PPF benefits specialist joining the Investment and we see this as an area where obtain a thorough oversight of and the cost of running the PPF in four ways: Team to support our Head of we can have the most influence. our portfolios in relation to ESG 11% ESG. We have also expanded We have also established a set of risks and opportunities, we are our access to available ESG data, minimum requirements around ESG investing significantly in expertise to insights and analytics, which allow integration and stewardship, and monitor these portfolios ourselves. Split of funding sources us to better track, monitor and will ensure that our expectations Whilst challenging, we recognise Assets from pension schemes ultimately report on various risks are met in order to continue that a tailored approach is often transferred to us and opportunities. Applying the relationships with our external necessary as different schemes The return we make on our TCFD’s recommendations has been managers. will have different characteristics 22.5% 40.5% a key area of focus, as we continue and expectations. The momentum investments to integrate climate-related risk around ESG integration has built The levy we charge on eligible assessment and management. in recent years, yet we are still in pension schemes the early stages of the journey, and Recovered assets we secure recognise that all partners must from insolvent employers work together to deliver on this successfully. We have £32 billion in our investment portfolio Barry Kenneth(31 March 2019) which is continually growing, and is 26% currently managed both internally and externally. Source: The PPF

12 www.ppf.co.uk Responsible Investment Report 2019/20 13 The foundations of our RI principles A Embedding our core focus on risk management. It covers ppr our processes and procedures, PRI’s six Principles Our climate change policy governs our principles and actions around climate change related risks relevant to oa beliefs and investment our investments. The policy was formally approved by the Board in 2019 and can be accessed on our website. c principles into our RI while also facilitating flexibility and for Responsible Throughout this report, we have provided signposts for each aspect of how we are implementing our climate h longevity, to enable us to keep pace Investment change policy: strategy with evolving regulation in this space. The PPF was an early signatory We view ESG factors as the Climate change policy to the PRI back in 2007, and has interaction of our investments Principle 1: We will incorporate (TCFD pillar*) Location considered the PRI’s six Principles with: ESG issues into investment analysis and decision-making Climate-related investment Our core RI beliefs (12); Managing climate change risks and opportunities as a base for guiding our own core - the physical environment and processes. beliefs (G) (30-37) RI beliefs and investment principles. climate (E); These beliefs are also embedded Assessment of Use of ESG data to identify and manage ESG risks (16, 31-32); Managing E Principle 2: We will be active x in our Statement of Investment - communities, workforces, wider climate-related impacts climate change risks and opportunities (30-37) e owners and incorporate ESG c u Principles. Our RI strategy and society and economies (S); on investments (S) t framework was further developed issues into our ownership ion in 2018/19. It incorporates ESG - governance structures of the policies and practices. risks and opportunities across our organisations and markets we External manager expectations Our RI approach (14-17); Working with our external managers (15-16, 20); investment process, with an essential invest in (G). Principle 3: We will seek around climate-related Managing climate change risks and opportunities (30-37); Climate change appropriate disclosure on ESG stewardship (RM) stewardship in risk management (32-33); Roadmap: assessing climate exposure issues by the entities in which (30-31) Our RI strategy we invest. Collaboration with peers Engagement with industry and collaborative initiatives (17); Collaborative Our core RI beliefs Principle 4: We will promote and industry initiatives (RM) efforts to engage and improve RI standards across asset classes (28-29); acceptance and implementation Managing climate change risks and opportunities (30-37) 1. By acting as a responsible and vigilant asset owner, we can protect L o of the Principles within the o and enhance the value of our investments. Reporting and engagement on Managing climate change risks and opportunities (30-37); Climate-related k investment industry. in climate-related activities (M&T) disclosure (35) g f o 2. ESG factors can have an impact on the performance of our r Principle 5: We will work w investments, and the management of ESG risks and exploitation of *G – Governance; S – Strategy; RM – Risk Management; M&T - Metrics & Targets ar ESG opportunities can, particularly for a portfolio-wide issue like together to enhance our d climate change, add value to our portfolio. effectiveness in implementing the Principles. Under stewardship, our minimum One aspect we recognise as an area Principle 6: We will each report standards policy sets out our for improvement is sharing what on our activities and progress requirements for responsible we do more widely, which we are RI Framework towards implementing the conduct from our underlying issuers addressing in a number of ways, Principles. and external managers, which including the publication of this are aligned with internationally report. Governance & Strategic Risk Metrics & recognised norms or international Accountability Direction & Management Transparency conventions for controversial Policy activities that are ratified into UK law. A new stewardship policy is also Priorities being developed with a bespoke voting and engagement focus for certain themes. Finally, for reporting, we are a strong advocate for transparency across Climate Change Stewardship Reporting the entire investment value chain and a supporter of several disclosure initiatives, including the TCFD and Underneath the RI framework, we have identified three key priorities: Climate the CDP, where we are an Investor Change, Stewardship, and Reporting. To support these priorities, we apply member. We were pleased to receive a set of specific policies, reviewed annually, to ensure that emerging best an assessment score of A+ for the practices are considered. Strategy & Governance module in the 2019 PRI reporting cycle, and A across nearly all other modules.

12www.ppf.co.ukResponsible Investment Report 2019/20 13 The foundations of our RI principles A Embedding our core focus on risk management. It covers ppr our processes and procedures, PRI’s six Principles Our climate change policy governs our principles and actions around climate change related risks relevant to oa beliefs and investment our investments. The policy was formally approved by the Board in 2019 and can be accessed on our website. c principles into our RI while also facilitating flexibility and for Responsible Throughout this report, we have provided signposts for each aspect of how we are implementing our climate h longevity, to enable us to keep pace Investmentchange policy: strategywith evolving regulation in this space. The PPF was an early signatory We view ESG factors as the Climate change policy to the PRI back in 2007, and has interaction of our investments Principle 1: We will incorporate (TCFD pillar*)Location considered the PRI’s six Principles with:ESG issues into investment analysis and decision-making Climate-related investment Our core RI beliefs (12); Managing climate change risks and opportunities as a base for guiding our own core - the physical environment and processes.beliefs (G)(30-37) RI beliefs and investment principles. climate (E); These beliefs are also embedded Assessment of Use of ESG data to identify and manage ESG risks (16, 31-32); Managing E Principle 2: We will be active x in our Statement of Investment - communities, workforces, wider climate-related impacts climate change risks and opportunities (30-37) e owners and incorporate ESG c u Principles. Our RI strategy and society and economies (S);on investments (S) t framework was further developed issues into our ownership ion in 2018/19. It incorporates ESG - governance structures of the policies and practices. risks and opportunities across our organisations and markets we External manager expectations Our RI approach (14-17); Working with our external managers (15-16, 20); investment process, with an essential invest in (G).Principle 3: We will seek around climate-related Managing climate change risks and opportunities (30-37); Climate change appropriate disclosure on ESG stewardship (RM) stewardship in risk management (32-33); Roadmap: assessing climate exposure issues by the entities in which (30-31) Our RI strategy we invest.Collaboration with peers Engagement with industry and collaborative initiatives (17); Collaborative Our core RI beliefsPrinciple 4: We will promote and industry initiatives (RM)efforts to engage and improve RI standards across asset classes (28-29); acceptance and implementation Managing climate change risks and opportunities (30-37) 1. By acting as a responsible and vigilant asset owner, we can protect L o of the Principles within the o and enhance the value of our investments.Reporting and engagement on Managing climate change risks and opportunities (30-37); Climate-related k investment industry. in climate-related activities (M&T) disclosure (35) g f o 2. ESG factors can have an impact on the performance of our r Principle 5: We will work w investments, and the management of ESG risks and exploitation of *G – Governance; S – Strategy; RM – Risk Management; M&T - Metrics & Targets ar ESG opportunities can, particularly for a portfolio-wide issue like together to enhance our d climate change, add value to our portfolio.effectiveness in implementing the Principles. Under stewardship, our minimum One aspect we recognise as an area Principle 6: We will each report standards policy sets out our for improvement is sharing what on our activities and progress requirements for responsible we do more widely, which we are RI Frameworktowards implementing the conduct from our underlying issuers addressing in a number of ways, Principles. and external managers, which including the publication of this are aligned with internationally report. Governance & Strategic RiskMetrics & recognised norms or international AccountabilityDirection & ManagementTransparencyconventions for controversial Policy activities that are ratified into UK law. A new stewardship policy is also Priorities being developed with a bespoke voting and engagement focus for certain themes. Finally, for reporting, we are a strong advocate for transparency across Climate ChangeStewardshipReportingthe entire investment value chain and a supporter of several disclosure initiatives, including the TCFD and Underneath the RI framework, we have identified three key priorities: Climate the CDP, where we are an Investor Change, Stewardship, and Reporting. To support these priorities, we apply member. We were pleased to receive a set of specific policies, reviewed annually, to ensure that emerging best an assessment score of A+ for the practices are considered. Strategy & Governance module in the 2019 PRI reporting cycle, and A across nearly all other modules.

14 www.ppf.co.uk Responsible Investment Report 2019/20 15 Our RI approach A ppr RI criteria and ESG considerations as part of our investment process oa c h Phase Request for Selection/ Appointment Post-funding proposal/ due diligence identification ESG Evidence of firm-level Ensure ESG Binding ESG and Ongoing monitoring requirement and strategy-level ESG processes are in climate-risk clauses and engagement with policy; PRI support; place, appropriate inclusion in legal external managers; E and capabilities or industry guidelines are documentation (e.g. regular fund-level x e c resources for ESG followed and reporting IMAs, LPAs, side ESG, carbon and u t integration. is available. letters). stewardship reporting; ion commitment to continuous improvement. ESG integration ESG integration (including climate External manager selection Our RI strategy is primarily focused change) is achieved by engaging with and due diligence on integrating material ESG issues and advancing the ESG practices Before we appoint external of our external managers and L into our investment process, which o managers, we carry out extensive o underlying issuers, rather than k we believe allows us to make more due diligence on their RI policies in divesting. As a large and diversified g informed decisions and enhances the and approach to ESG integration, f asset owner, we have the opportunity o r RI governance at the PPF value of our assets. Since 2007, we which not only includes minimum w have applied Principles 1 and 2 of the to encourage improvements in ar Inadequate governance is often a factor in schemes entering the PPF, therefore we have a responsibility to PRI’s Six Principles for Responsible ESG integration from the top down requirements that they must meet, d exemplify good governance on behalf of our members and levy payers. and bottom up. We expect our but also a consideration of how they Investment (see page 12) as a external managers to integrate all might go beyond those minimum benchmark for integrating ESG across relevant material factors into their standards. We have also integrated PPF Board Highest governing body with oversight of RI all asset classes and markets in which investment analysis and decisions, considerations on diversity and (including climate-related) issues. we invest. We take a materiality-based and demonstrate active stewardship. inclusion policies and initiatives approach to relevant ESG factors, Our expectations vary between within the external manager’s firm. and give particular consideration to different asset classes, depending We ensure that appropriate RI climate change (see page 13 Climate on relevance (such as time horizons clauses are incorporated into all Investment Responsibility for developing and maintaining the Fund’s change policy – assessment for or types of instruments used) and investment management agreements Committee (IC) RI principles and policies (including climate-related) is further information). current best practice. and side letters. delegated to the IC. Investment Team Led by the Chief Investment Officer (CIO). Responsibility for ensuring adherence to the RI framework and associated ESG Team policies (including the integration of climate change) across all asset classes, both internally and externally managed. The ESG Team, as part of the Investment Team, provides support and expertise, oversees appropriate implementation of the RI framework, engages with portfolio managers, and monitors investments for ESG risks and opportunities (including climate-related).

14www.ppf.co.ukResponsible Investment Report 2019/20 15 Our RI approach A ppr RI criteria and ESG considerations as part of our investment process oa c h Phase Request for Selection/ Appointment Post-funding proposal/ due diligence identification ESG Evidence of firm-level Ensure ESG Binding ESG and Ongoing monitoring requirement and strategy-level ESG processes are in climate-risk clauses and engagement with policy; PRI support; place, appropriate inclusion in legal external managers; E and capabilities or industry guidelines are documentation (e.g. regular fund-level x e c resources for ESG followed and reporting IMAs, LPAs, side ESG, carbon and u t integration. is available. letters). stewardship reporting; ion commitment to continuous improvement. ESG integration ESG integration (including climate External manager selection Our RI strategy is primarily focused change) is achieved by engaging with and due diligence on integrating material ESG issues and advancing the ESG practices Before we appoint external of our external managers and L into our investment process, which o managers, we carry out extensive o underlying issuers, rather than k we believe allows us to make more due diligence on their RI policies in divesting. As a large and diversified g informed decisions and enhances the and approach to ESG integration, f asset owner, we have the opportunity o r RI governance at the PPF value of our assets. Since 2007, we which not only includes minimum w have applied Principles 1 and 2 of the to encourage improvements in ar Inadequate governance is often a factor in schemes entering the PPF, therefore we have a responsibility to PRI’s Six Principles for Responsible ESG integration from the top down requirements that they must meet, d exemplify good governance on behalf of our members and levy payers.and bottom up. We expect our but also a consideration of how they Investment (see page 12) as a external managers to integrate all might go beyond those minimum benchmark for integrating ESG across relevant material factors into their standards. We have also integrated PPF BoardHighest governing body with oversight of RI all asset classes and markets in which investment analysis and decisions, considerations on diversity and (including climate-related) issues.we invest. We take a materiality-based and demonstrate active stewardship. inclusion policies and initiatives approach to relevant ESG factors, Our expectations vary between within the external manager’s firm. and give particular consideration to different asset classes, depending We ensure that appropriate RI climate change (see page 13 Climate on relevance (such as time horizons clauses are incorporated into all Investment Responsibility for developing and maintaining the Fund’s change policy – assessment for or types of instruments used) and investment management agreements Committee (IC)RI principles and policies (including climate-related) is further information).current best practice.and side letters. delegated to the IC. Investment TeamLed by the Chief Investment Officer (CIO). Responsibility for ensuring adherence to the RI framework and associated ESG Teampolicies (including the integration of climate change) across all asset classes, both internally and externally managed. The ESG Team, as part of the Investment Team, provides support and expertise, oversees appropriate implementation of the RI framework, engages with portfolio managers, and monitors investments for ESG risks and opportunities (including climate-related).

16 www.ppf.co.uk Responsible Investment Report 2019/20 17 Our RI approach – continued A Ongoing monitoring and rating We have an internal RI policy, as well Use of ESG data to identify ppr of external manager mandates as guidance and implementation and manage ESG risks oa c When monitoring our external documents which set out our At a strategy and individual portfolio h managers, we assign to them an ESG expectations of external managers level, ESG risks (including climate- rating which forms part of a wider and in various asset classes. These related risks) are identified internally integrated performance-monitoring are reviewed and updated when using monitoring processes, tools, framework. The ESG rating (specific to new insights and best practices data and systems – enabling us to asset class and strategy) scores our are available, such as when new engage with our external managers external managers across a number guidelines are issued by the PRI around risk identification and of areas, such as RI governance, or other organisations. These management activities. ESG data alignment and resources; integration documents support the assessment is available through our portfolio of our external managers, and E of ESG factors within investment management systems, and we x inform our due diligence process e c analysis and decision-making; are developing our processes u and requirements for incorporating t stewardship; and reporting. All ESG into fund terms. When for monitoring ESG and climate- ion external managers are required to communicating our expectations to related risks at a fund, asset class report material ESG issues alongside managers, the feedback is tailored and strategy level as part of risk their investment performance, and RI to the areas where we see scope for reporting (see page 30 for more on is a standing agenda item in external improvement. our activities around climate-related manager review meetings. strategy and risk identification). Exercising our ownership is currently operationally complex. For rights such as shareholder asset classes outside listed equities, rights and voting such as listed credit, alternative credit L and private equity, our external o o Active ownership through share k managers also report to us on in voting and issuer engagement is a g stewardship activities and progress f key part of our role as a responsible o r (see more on voting activity in 2019 w asset owner. It is an essential risk on page 27 and climate-related voting ar management tool that ensures that on page 33). d boards are accountable and are fulfilling their stewardship obligations. While these activities are outsourced, We welcome the enhanced UK we maintain oversight of our external Stewardship Code (January 2020) agents by monitoring their voting and and will develop a new stewardship engagement practices in order to policy and enhance our stewardship enhance the quality and quantity of practices to align with the Code. We their stewardship activities. For high are supportive of its aim to further profile issues, where possible, we will improve the quality of engagement enquire about our external managers’ between asset owners, external voting intentions ahead of AGMs. managers and issuers, and the emphasis it has on establishing Engagement with industry strong and transparent corporate and collaborative initiatives governance practices. We participate in industry-wide Within our global listed equity collaborative initiatives to help portfolio, our external agents develop best practice and to ensure (managers and other vendors) vote that our own RI standards are aligned and monitor portfolio companies for with industry standards. On pages ESG risks – if concerns arise, they will 20, 28-29, we outline outcomes of engage with issuers on our behalf. engagement with external managers, For our segregated equity portfolios, industry and collaborative initiatives we have appointed a specialist designed to improve or set RI Engagement & Voting provider to standards across asset classes. support our stewardship activities. For pooled equity funds, we rely on the relevant external manager’s stewardship activities, since extracting voting rights from pooled investments

16www.ppf.co.ukResponsible Investment Report 2019/20 17 Our RI approach – continued A Ongoing monitoring and rating We have an internal RI policy, as well Use of ESG data to identify ppr of external manager mandates as guidance and implementation and manage ESG risks oa c When monitoring our external documents which set out our At a strategy and individual portfolio h managers, we assign to them an ESG expectations of external managers level, ESG risks (including climate- rating which forms part of a wider and in various asset classes. These related risks) are identified internally integrated performance-monitoring are reviewed and updated when using monitoring processes, tools, framework. The ESG rating (specific to new insights and best practices data and systems – enabling us to asset class and strategy) scores our are available, such as when new engage with our external managers external managers across a number guidelines are issued by the PRI around risk identification and of areas, such as RI governance, or other organisations. These management activities. ESG data alignment and resources; integration documents support the assessment is available through our portfolio of our external managers, and E of ESG factors within investment management systems, and we x inform our due diligence process e c analysis and decision-making; are developing our processes u and requirements for incorporating t stewardship; and reporting. All ESG into fund terms. When for monitoring ESG and climate- ion external managers are required to communicating our expectations to related risks at a fund, asset class report material ESG issues alongside managers, the feedback is tailored and strategy level as part of risk their investment performance, and RI to the areas where we see scope for reporting (see page 30 for more on is a standing agenda item in external improvement. our activities around climate-related manager review meetings. strategy and risk identification). Exercising our ownership is currently operationally complex. For rights such as shareholder asset classes outside listed equities, rights and voting such as listed credit, alternative credit L and private equity, our external o o Active ownership through share k managers also report to us on in voting and issuer engagement is a g stewardship activities and progress f key part of our role as a responsible o r (see more on voting activity in 2019 w asset owner. It is an essential risk on page 27 and climate-related voting ar management tool that ensures that on page 33). d boards are accountable and are fulfilling their stewardship obligations. While these activities are outsourced, We welcome the enhanced UK we maintain oversight of our external Stewardship Code (January 2020) agents by monitoring their voting and and will develop a new stewardship engagement practices in order to policy and enhance our stewardship enhance the quality and quantity of practices to align with the Code. We their stewardship activities. For high are supportive of its aim to further profile issues, where possible, we will improve the quality of engagement enquire about our external managers’ between asset owners, external voting intentions ahead of AGMs. managers and issuers, and the emphasis it has on establishing Engagement with industry strong and transparent corporate and collaborative initiatives governance practices. We participate in industry-wide Within our global listed equity collaborative initiatives to help portfolio, our external agents develop best practice and to ensure (managers and other vendors) vote that our own RI standards are aligned and monitor portfolio companies for with industry standards. On pages ESG risks – if concerns arise, they will 20, 28-29, we outline outcomes of engage with issuers on our behalf. engagement with external managers, For our segregated equity portfolios, industry and collaborative initiatives we have appointed a specialist designed to improve or set RI Engagement & Voting provider to standards across asset classes. support our stewardship activities. For pooled equity funds, we rely on the relevant external manager’s stewardship activities, since extracting voting rights from pooled investments

18 www.ppf.co.uk Responsible Investment Report 2019/20 19 A p p r o Execution ach E xe c u t io n L o o k in g f o r w ar d

18www.ppf.co.ukResponsible Investment Report 2019/20 19 A p p r o Execution ach E xe c u t io n L o o k in g f o r w ar d

20 www.ppf.co.uk Responsible Investment Report 2019/20 21 Being active owners A p Working with our external managers Stewardship outcomes 2019-2021 engagement themes of our external provider p r o From a stewardship perspective, we engage directly with We engage with our external managers and expect ach our external managers. Robust ESG data and tools allow them to monitor and influence underlying issuers for Environment Social Strategy, risk and Governance us to better track and manage our risk exposure, report both equity and debt positions. We also expect them to • Climate change • Conduct, culture communication • Shareholder transparently to our stakeholders, and communicate exercise voting rights on our behalf, with the exception • Natural resource and ethics • Risk management protection and rights regularly with our external managers. of our segregated equities where we engage with stewardship • Human capital • Corporate reporting • Executive companies and vote directly via our external provider. • Pollution, waste and management • Business purpose remuneration In late 2019, we expanded the ESG data we receive from The overarching themes that we expect our external circular economy • Human and and strategy • Board effectiveness external providers to include a wider variety of metrics at agents to engage on include climate change, human labour rights both a portfolio and issuer level, including climate-related capital, diversity and inclusion, board composition and metrics (see pages 32, 35, Managing climate change risks executive remuneration. E and opportunities for more detail). xe c u Segregated equities engagement strategy t Engagement milestone process of our external provider io We continuously monitor our external managers on their 2019-2021 n overall ESG performance and stewardship activities, and The following section focuses on the progress of our 4 offer guidance and support on their ESG practices, aiming external provider with respect to our segregated to elevate the industry to a more common understanding equity mandates, as this is where we receive the most The company of RI. Development plans for external managers that do comprehensive reporting. However, a key action for the 3 implements a strategy not meet our requirements are implemented. We ensure coming year is to work with our external managers of The company develops or measures to that these plans are meaningful and effective, and if signs pooled funds to improve the quality and comparability 2 a credible strategy to address the concern. of improvement or genuine action towards ESG progress of reporting. achieve the objective, or are not made over a specified time period, we will re- 1 The company stretching targets are set evaluate our relationship. acknowledges the issue L Our external provider for stewardship of our segregated to address the concern. o as a serious investor o Our concern is raised k equity mandates has created a 2019-2021 Engagement concern, worthy of a in with the company at g & Voting roadmap to engage with companies. The f response. o the appropriate level. r Case study roadmap identifies 12 themes across environment; w social; strategy, risk and communication; and ar Encouraging external manager governance, which cover material issues relevant to d industry collaboration through companies in all regions and sectors. engagement Engagement with investee companies happens in Progress stages, following specific milestones. Engagement can often take place over a multi-year period, so milestones Segregated equities engagement highlights We put PRI Principle 4, ‘promote acceptance track progress that are related to objectives set at the https://ppf.co.uk/reporting-investing-transparently Segregated portfolios and implementation of the Principles within beginning of our interactions, which can vary depending Over the 2019 calendar year, we engaged with 136 engagement by region the investment industry’, into practice by on the types of issues raised. companies in our segregated equity portfolios on 426 encouraging our external managers to issues and objectives through our external provider. 10% become signatories. Actively demonstrating The following charts summarise our activities by region the benefits of PRI membership, among other Case study and the most common topics that we engaged on. industry and collaboration initiatives such as Institutional Limited Partners Association Alternatives external manager (ILPA), GRESB, TCFD and Climate Action 26% 36% 100+, has seen a number of our external increases ESG integration managers in the Alternatives space becoming signatories to the PRI. Through continuous engagement, a long-standing US Alternatives external manager created a new vehicle designed to allow our RI expectations to be incorporated 27% within our mandate with them. North America Europe & UK Developed Asia (inc Aus & NZ) Emerging markets Source: EOS at Federated Hermes (external provider) 2019

20www.ppf.co.ukResponsible Investment Report 2019/20 21 Being active owners A p Working with our external managers Stewardship outcomes 2019-2021 engagement themes of our external provider p r o From a stewardship perspective, we engage directly with We engage with our external managers and expect ach our external managers. Robust ESG data and tools allow them to monitor and influence underlying issuers for EnvironmentSocialStrategy, risk and Governance us to better track and manage our risk exposure, report both equity and debt positions. We also expect them to • Climate change • Conduct, culture communication• Shareholder transparently to our stakeholders, and communicate exercise voting rights on our behalf, with the exception • Natural resource and ethics• Risk managementprotection and rights regularly with our external managers. of our segregated equities where we engage with stewardship• Human capital • Corporate reporting• Executive companies and vote directly via our external provider. • Pollution, waste and management • Business purpose remuneration In late 2019, we expanded the ESG data we receive from The overarching themes that we expect our external circular economy• Human and and strategy• Board effectiveness external providers to include a wider variety of metrics at agents to engage on include climate change, human labour rights both a portfolio and issuer level, including climate-related capital, diversity and inclusion, board composition and metrics (see pages 32, 35, Managing climate change risks executive remuneration. E and opportunities for more detail). xe c u Segregated equities engagement strategy t Engagement milestone process of our external provider io We continuously monitor our external managers on their 2019-2021 n overall ESG performance and stewardship activities, and The following section focuses on the progress of our 4 offer guidance and support on their ESG practices, aiming external provider with respect to our segregated to elevate the industry to a more common understanding equity mandates, as this is where we receive the most The company of RI. Development plans for external managers that do comprehensive reporting. However, a key action for the 3implements a strategy not meet our requirements are implemented. We ensure coming year is to work with our external managers of The company develops or measures to that these plans are meaningful and effective, and if signs pooled funds to improve the quality and comparability 2a credible strategy to address the concern. of improvement or genuine action towards ESG progress of reporting. achieve the objective, or are not made over a specified time period, we will re-1The company stretching targets are set evaluate our relationship. acknowledges the issue L Our external provider for stewardship of our segregated to address the concern. o as a serious investor o Our concern is raised k equity mandates has created a 2019-2021 Engagement concern, worthy of a in with the company at g & Voting roadmap to engage with companies. The f response. o the appropriate level. r Case studyroadmap identifies 12 themes across environment; w social; strategy, risk and communication; and ar Encouraging external manager governance, which cover material issues relevant to d industry collaboration through companies in all regions and sectors. engagementEngagement with investee companies happens in Progress stages, following specific milestones. Engagement can often take place over a multi-year period, so milestones Segregated equities engagement highlights We put PRI Principle 4, ‘promote acceptance track progress that are related to objectives set at the https://ppf.co.uk/reporting-investing-transparentlySegregated portfolios and implementation of the Principles within beginning of our interactions, which can vary depending Over the 2019 calendar year, we engaged with 136 engagement by region the investment industry’, into practice by on the types of issues raised. companies in our segregated equity portfolios on 426 encouraging our external managers to issues and objectives through our external provider. 10% become signatories. Actively demonstrating The following charts summarise our activities by region the benefits of PRI membership, among other Case studyand the most common topics that we engaged on. industry and collaboration initiatives such as Institutional Limited Partners Association Alternatives external manager (ILPA), GRESB, TCFD and Climate Action 26% 36% 100+, has seen a number of our external increases ESG integration managers in the Alternatives space becoming signatories to the PRI. Through continuous engagement, a long-standing US Alternatives external manager created a new vehicle designed to allow our RI expectations to be incorporated 27% within our mandate with them. North America Europe & UK Developed Asia (inc Aus & NZ) Emerging markets Source: EOS at Federated Hermes (external provider) 2019

22 www.ppf.co.uk Responsible Investment Report 2019/20 23 Being active owners – continued A p Summary of engagement themes p Segregated portfolios engagement by types of issue r o in 2019/20 ach Executive remuneration (45%) Board diversity (24%) 18% Engagement programme companies Human rights (22%) 192 42% # of # of issues % of objectives objectives engaged on Business strategy (37%) (related to) # of objectives completed 19% objectives objectives with or engaged engaged progress discontinued E Reporting & disclosure (26%) xe c Environment 90 62 47% 6 u t io Social 77 37 57% 9 51% n Climate change (63%) 21% Governance 179 67 54% 10 objectives with progress Governance Strategy, risk & Environmental communication 80 26 42% 5 Total 426* 192** 51% 30 Strategy, Risk & Communication Social & Ethical Source: EOS at Federated Hermes (external provider) 2019 * We measure engagement outcomes for specifically set objectives, while engagement happens on a broader set of identified issues of concern within ESG themes. Source: EOS at Federated Hermes (external provider) 2019 L ** Total number of objectives is higher than total number of companies engaged due to more o o k than one objective per company for some companies. in g Segregated equities f Companies engaged by number of interactions o r engagement outcomes and w Board composition and In support of the ‘30% Club’, our ar interaction intensity diversity and inclusion external provider developed a board- d Engagement differs between 71 level diversity recommendation to companies – some need multiple Within our segregated equity have 30 per cent women on FTSE engagements before they take action, mandates, board composition and 100 boards and 25 per cent on FTSE while others are responsive after very diversity accounted for almost a 250 boards (read about voting on minimal interaction. We are pleased quarter of governance-related board composition and diversity on to report that, as a result of successful engagements undertaken by our page 27). engagement, at least one milestone 32 33 external provider on our behalf. was moved forward for around 50 per Number of companies Through engagement, we seek We also support the progress cent of our objectives. to underline the importance of of board and gender diversity in 1 interaction 2 or 3 4+ diversity. This includes gender, age, other jurisdictions, for instance, the interactions interactions ethnicity, nationality, background, publication of the German Corporate skills and experience to improve Governance Principles mirrors the Companies engaged by number of interactions decision-making and avoid goal of the ‘30% Club’. Currently, only groupthink. Good governance 8 per cent of German companies 36 features significantly in our have more than one woman on the engagement, as it is often the first executive board. Two thirds still step towards addressing social or have no female board members. In 29 environmental issues. the US, we also continued to push our expectations for board diversity 21 across a number of dimensions. Engagement progress 11 Milestones seeing positive progress Governance Social Environment Strategy, Risk & Communication Source: EOS at Federated Hermes (external provider) 2019

22www.ppf.co.ukResponsible Investment Report 2019/20 23 Being active owners – continued A p Summary of engagement themes p Segregated portfolios engagement by types of issue r o in 2019/20 ach Executive remuneration (45%) Board diversity (24%) 18% Engagement programme companies Human rights (22%) 192 42% # of # of issues % of objectives objectives engaged on Business strategy (37%) (related to) # of objectives completed 19% objectives objectives with or engaged engaged progress discontinued E Reporting & disclosure (26%) xe c Environment 90 62 47% 6 u t io Social 77 37 57% 9 51% n Climate change (63%)21%Governance 179 67 54% 10 objectives with progress Governance Strategy, risk & Environmental communication 80 26 42% 5 Total 426* 192** 51% 30 Strategy, Risk & Communication Social & EthicalSource: EOS at Federated Hermes (external provider) 2019 * We measure engagement outcomes for specifically set objectives, while engagement happens on a broader set of identified issues of concern within ESG themes. Source: EOS at Federated Hermes (external provider) 2019 L ** Total number of objectives is higher than total number of companies engaged due to more o o k than one objective per company for some companies. in g Segregated equities f Companies engaged by number of interactions o r engagement outcomes and w Board composition and In support of the ‘30% Club’, our ar interaction intensity diversity and inclusion external provider developed a board- d Engagement differs between 71 level diversity recommendation to companies – some need multiple Within our segregated equity have 30 per cent women on FTSE engagements before they take action, mandates, board composition and 100 boards and 25 per cent on FTSE while others are responsive after very diversity accounted for almost a 250 boards (read about voting on minimal interaction. We are pleased quarter of governance-related board composition and diversity on to report that, as a result of successful engagements undertaken by our page 27). engagement, at least one milestone 3233external provider on our behalf. was moved forward for around 50 per Number of companiesThrough engagement, we seek We also support the progress cent of our objectives. to underline the importance of of board and gender diversity in 1 interaction2 or 3 4+ diversity. This includes gender, age, other jurisdictions, for instance, the interactionsinteractionsethnicity, nationality, background, publication of the German Corporate skills and experience to improve Governance Principles mirrors the Companies engaged by number of interactionsdecision-making and avoid goal of the ‘30% Club’. Currently, only groupthink. Good governance 8 per cent of German companies 36 features significantly in our have more than one woman on the engagement, as it is often the first executive board. Two thirds still step towards addressing social or have no female board members. In 29 environmental issues. the US, we also continued to push our expectations for board diversity 21 across a number of dimensions. Engagement progress11 Milestones seeing positive progress Governance Social Environment Strategy, Risk & Communication Source: EOS at Federated Hermes (external provider) 2019

24 www.ppf.co.uk Responsible Investment Report 2019/20 25 Being active owners – continued A p p r o Case study ach Continuous engagement with miners on board diversity Through our external provider, we have been engaging with a multinational mining company on a range of themes, from climate change and natural resource E xe use to executive remuneration and risk c u t management. In 2017, concerns included io direct engagement with the chairman on n board structure changes, which resulted in the appointment of two female directors to the 12-member board. Furthermore, in early 2018, the company appointed a new female non-executive director in a step towards 33 per cent female representation. A minimum target was also recommended for 2020, with continued engagement L o from our external provider on this. o k in g f o r Case study w Human capital and and informally) with employees to include a list of companies required ar Corporate governance engagement in Asia corporate culture further understand results. Whilst to comply with the MSA, regardless d Within our passive equity mandates, culture-related metrics and targets of whether they had submitted a we place a high level of scrutiny on are challenging to determine, we compliant statement or not. They Corporate governance can still South Korea: In 2019 our our external managers’ stewardship are now seeing their inclusion in also supported the 'Find It, Fix It, vary across countries. Asset external provider joined the activities. During 2019, our external standardised frameworks such Prevent It' collaborative initiative to owners and external managers Asian Corporate Governance manager piloted a corporate as the Sustainability Accounting combat modern slavery, which called can play an effective role by Association’s (ACGA) culture and human capital project, Standards Board (SASB) and the on UK-listed companies to increase elevating their expectations coordinated engagement with to increase understanding and Workforce Disclosure Initiative. We their efforts to address this issue and assessment within the largest hope to see the emergence of best to support the provision of remedies on stewardship and ESG regulators, government and US technology companies. The practice over the next few years to victims. engagement in these countries. large companies from South project commenced by engaging as more standardised metrics are Japan: The introduction of the Korea on ways to improve with company executives who agreed, and our external manager In another engagement, as an Stewardship Code (2012) and corporate governance, such as had oversight for internal culture, will continue to engage with advisory committee member the Corporate Governance board role and composition, board oversight, strategy and technology companies on this issue. of the PRI’s cobalt supply chain Code (2015) in Japan has executive remuneration, capital remuneration. collaborative engagement, on our supported our engagement management and shareholder Forced labour and behalf, our external provider was protection. Although the responses from modern slavery the sole investor representative to with companies over the last the companies differed, some attend an Organisation for Economic few years. However, there are Our external provider responded to Co-operation and Development-led still some issues associated with commonalities were identified the UK Home Office's consultation (OECD) event and roundtable in the board composition and diversity, during the process. For example, all on potential revisions to the UK’s Democratic Republic of Congo. The and our external provider’s companies conducted engagement Modern Slavery Act (MSA) in 2019 event allowed them to see first- engagements with Japanese surveys with their staff, and most and argued for a requirement to hand the human rights challenges companies are often centred on passed aggregated engagement report on recommended areas, presented in the mining sector and this issue. results to the board, but very instead of adopting a 'comply or share perspectives with local and few gave examples of tangible explain' approach. They supported international stakeholders. board actions arising from survey the creation of a central registry outcomes. This is inconsistent with to enable stakeholders, including our external manager’s expectation investors, to access companies' for boards to engage (formally modern slavery statements, to

24www.ppf.co.ukResponsible Investment Report 2019/20 25 Being active owners – continued A p p r o Case study ach Continuous engagement with miners on board diversity Through our external provider, we have been engaging with a multinational mining company on a range of themes, from climate change and natural resource E xe use to executive remuneration and risk c u t management. In 2017, concerns included io direct engagement with the chairman on n board structure changes, which resulted in the appointment of two female directors to the 12-member board. Furthermore, in early 2018, the company appointed a new female non-executive director in a step towards 33 per cent female representation. A minimum target was also recommended for 2020, with continued engagement L o from our external provider on this. o k in g f o r Case study w Human capital and and informally) with employees to include a list of companies required ar Corporate governance engagement in Asia corporate culturefurther understand results. Whilst to comply with the MSA, regardless d Within our passive equity mandates, culture-related metrics and targets of whether they had submitted a we place a high level of scrutiny on are challenging to determine, we compliant statement or not. They Corporate governance can still South Korea: In 2019 our our external managers’ stewardship are now seeing their inclusion in also supported the 'Find It, Fix It, vary across countries. Asset external provider joined the activities. During 2019, our external standardised frameworks such Prevent It' collaborative initiative to owners and external managers Asian Corporate Governance manager piloted a corporate as the Sustainability Accounting combat modern slavery, which called can play an effective role by Association’s (ACGA) culture and human capital project, Standards Board (SASB) and the on UK-listed companies to increase elevating their expectations coordinated engagement with to increase understanding and Workforce Disclosure Initiative. We their efforts to address this issue and assessment within the largest hope to see the emergence of best to support the provision of remedies on stewardship and ESG regulators, government and US technology companies. The practice over the next few years to victims. engagement in these countries.large companies from South project commenced by engaging as more standardised metrics are Japan: The introduction of the Korea on ways to improve with company executives who agreed, and our external manager In another engagement, as an Stewardship Code (2012) and corporate governance, such as had oversight for internal culture, will continue to engage with advisory committee member the Corporate Governance board role and composition, board oversight, strategy and technology companies on this issue. of the PRI’s cobalt supply chain Code (2015) in Japan has executive remuneration, capital remuneration. collaborative engagement, on our supported our engagement management and shareholder Forced labour and behalf, our external provider was protection. Although the responses from modern slavery the sole investor representative to with companies over the last the companies differed, some attend an Organisation for Economic few years. However, there are Our external provider responded to Co-operation and Development-led still some issues associated with commonalities were identified the UK Home Office's consultation (OECD) event and roundtable in the board composition and diversity, during the process. For example, all on potential revisions to the UK’s Democratic Republic of Congo. The and our external provider’s companies conducted engagement Modern Slavery Act (MSA) in 2019 event allowed them to see first- engagements with Japanese surveys with their staff, and most and argued for a requirement to hand the human rights challenges companies are often centred on passed aggregated engagement report on recommended areas, presented in the mining sector and this issue. results to the board, but very instead of adopting a 'comply or share perspectives with local and few gave examples of tangible explain' approach. They supported international stakeholders. board actions arising from survey the creation of a central registry outcomes. This is inconsistent with to enable stakeholders, including our external manager’s expectation investors, to access companies' for boards to engage (formally modern slavery statements, to